Why the ‘war on inflation’ is over — even though the ‘experts’ don’t get it

[ad_1]

The war is over: not the war in Ukraine or Gaza – I mean the war on inflation.

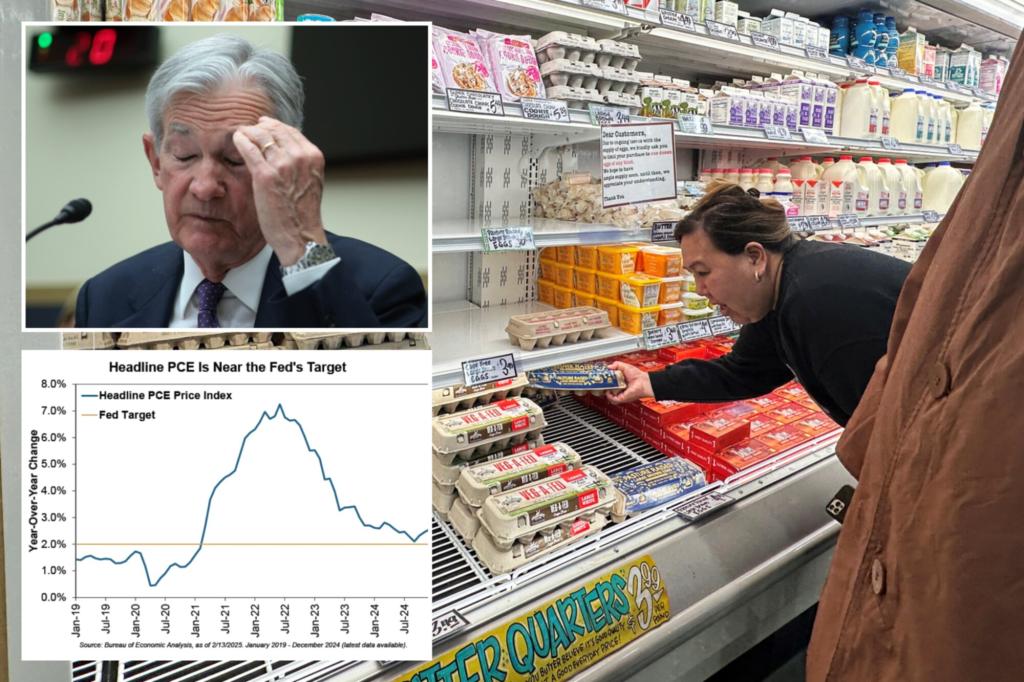

Shoppers, understandably, are still freaking out in the grocery aisles, most recently over egg prices. Meanwhile, economists, politicos and pundits continue to sweat allegedly “sticky” categories for goods and services and rising wages – especially after January’s Consumer Price Index accelerated.

They are all fighting the last war. How about you and your stock portfolio?

Yes, inflation has hammered households since 2021 and it has been horrific. The CPI ended January 23.4% above December 2019 – and that understates many shoppers’ experience – including yours, probably. It’s also true that the end of a military war doesn’t mean the destruction is somehow reversed.

The latter, unfortunately, is also the case with inflation. Prices and inflation are different. Inflation is the speed of rising prices — now 3% versus a year ago based on CPI. Prices overall don’t fall. Select categories may, but broadly falling prices – aka deflation – well, developed nations don’t do that. Why?

Real, deep deflation means depression – an even deadlier war. Reversing CPI’s post-pandemic rise means approximating 1929 – 1933’s deflation or the early 1920s’ post-World War I downturn. Is that really what you want? Didn’t think so. Winning the inflation war was never about lowering prices, but rather slowing their advance.

Last November, I detailed the reasons the Federal Reserve wants 2% ongoing annual inflation. Since peaking at 9.1% in June 2022, CPI irregularly cooled to January’s 3.0%. Despite all the yakking about acceleration, that’s 0.1% above December. A statistical blip. These measures aren’t that exact anyway.

Meanwhile, December’s “personal consumption expenditures price index,” the broader gauge the Fed actually targets, was 2.6% versus a year ago. Pundits shrieked that it was “stuck” above the 2% target, hyping every worrisome wiggle. But no evidence exists – none, zero, zip – that the Fed can fine-tune anything precisely.

Weirdly, “stubborn shelter” inflates CPI. But it’s mostly from the fictitious “owner’s equivalent rent” calculation – what goofball government statisticians guesstimate homeowners would pay to rent their own homes. No one pays this.

Excluding shelter, December CPI was 1.9% versus last year —including bird-flu-spiked eggs. The Fed doesn’t want it much lower. So, don’t expect it. But the “war” is over.

Inflation is simply a case of too much money chasing too few goods and services. It comes with a time lag – money supply growth rate exceeding GDP growth rate – and it’s always caused by the Fed, which never, ever takes responsibility.

During 2020’s COVID chaos, the Fed stupidly, bizarrely ballooned money supply. M4, the broadest gauge, soared 30.9% year over year in June 2020. M2, narrower, hit 26.6% in February 2021. Later, prices galloped.

The Fed has slowed down, now growing the money supply at 3.4% and 3.9%, respectively – below most years since the 1980s. Subtract from them about 2% annual GDP growth and you will see inflation ahead below 2%.

Worried about wage growth? I detailed last August exactly why it isn’t ever inflationary and can’t ever be. I won’t rehash that now – it was a whole long column, you can look it up. But economists, politicos and pundits seemingly never, ever learn.

How about President Trump’s tariffs? Again, the key here is that tariffs don’t affect money supply. Tariffs can make some prices rise – although far less and smaller than most think. Mainly, tariffs boost some prices while forcing others to fall. Tariffs channel demand, creating winners and losers.

Yes, tariffs are poor economic policy. But inflation isn’t why. Think of all that inflation we didn’t get with Trump’s first term tariffs.

So what’s the underappreciated, non-inflated truth for investors? Hate to burst some bubbles here, but market forecasting requires seeing something big that others don’t. Huffing and puffing about inflation alongside an army of “experts” won’t help.

The inflation war is over, full stop. Be bullish.

Ken Fisher is the founder and executive chairman of Fisher Investments, a four-time New York Times bestselling author, and regular columnist in 21 countries globally.

[ad_2]

Source link